A home loan software could be an extremely intimidating task, particularly through the a worldwide pandemic. But really, you keep curious if it’s worthy of postponing such a serious move.

For many people, mortgage loans are only an undeniable fact away from life. But, COVID-19 or perhaps not, you will find zero options however, to save conquering contrary to the latest.

Usually, the first area you have got to grapple with will probably be your credit rating. Should you want to qualify for home financing, you must meet the absolute minimum credit rating requisite. However, mortgages aren’t exactly tericans will probably don’t know what type of credit history they’re going to you prefer or the range out-of mortgage possibilities they’re able to like. This informative article hopes so you’re able to link one pit.

Today, let us put those individuals concerns out and put our very own thought hats on. It is the right time to find out the necessary information to find out that commonly produce home loan-in a position this 2021.

(Note: This short article is the FICO Score model since which is probably the most popular program by the credit agencies.)

Equity

A home loan was a secured particular mortgage. Of the secured, this means that for individuals who prevent settling your loan, the lender becomes one thing of yours inturn. In such a case, you eliminate ownership in your home, and also the mortgage lender deal they to recoup the losings.

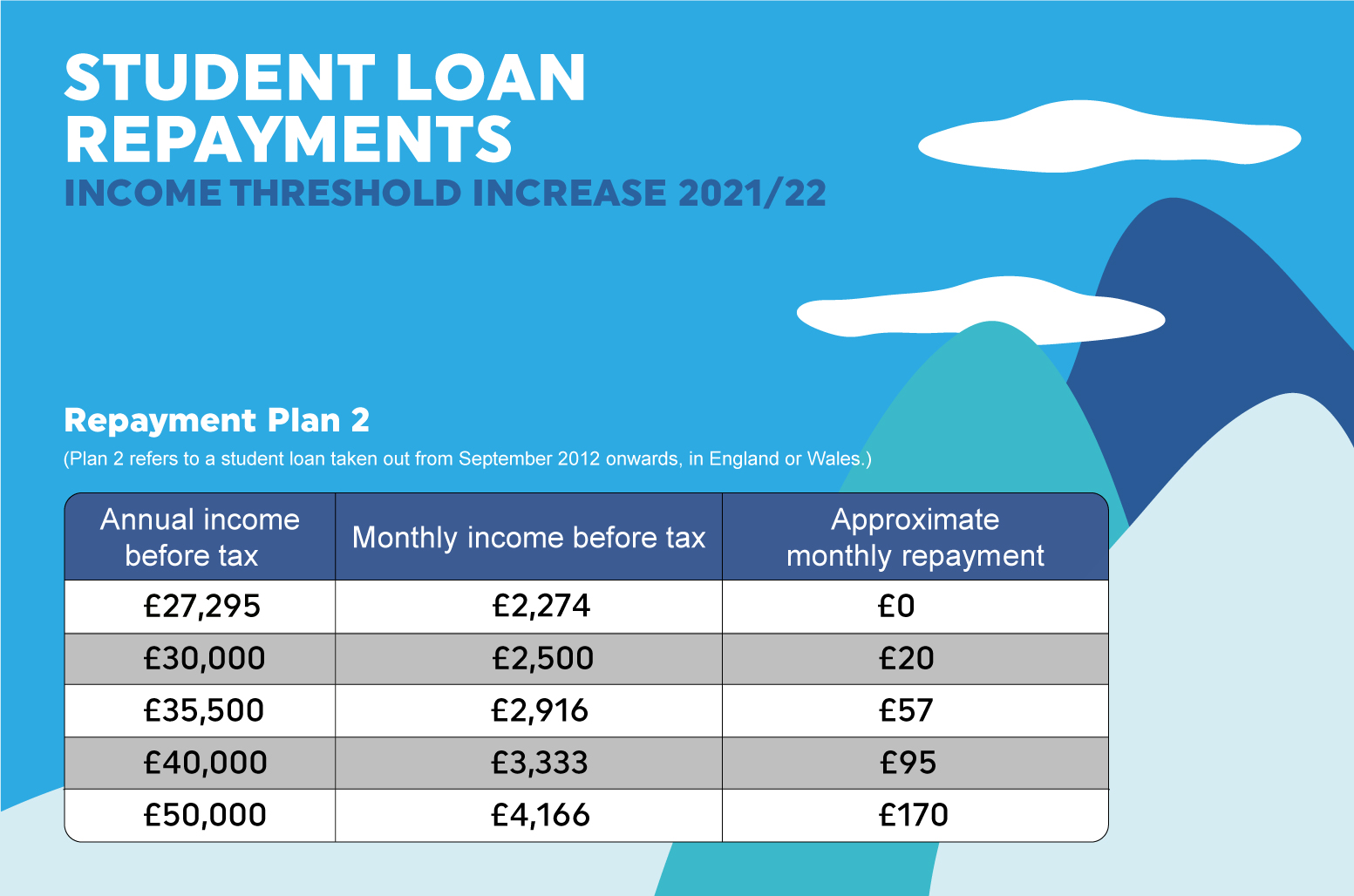

Fees

Amortization is even something which helps make mortgages more challenging for all those. You don’t pay-off the loan bank having a-one-go out fee. Instead, you will be making an initial commission filled with put and you will closing costs, and after that you rating billed having repayment per month. But you dont only separate your own full financing because of the count out of weeks you have to pay. Rates of interest change, and sometimes, mortgage insurance is in addition to inside. In place of almost every other money, mortgages deal with a great sum of https://paydayloanalabama.com/red-bay/ money repaid over a very long several months.

Just how amortization works, it could be tough to envision how much your residence usually in the course of time rates after you’ve generated the past percentage on the mortgage. This is exactly why it’s critical to choose the best loan words right off the bat, avoid paying for insurance rates, to make the most significant deposit your savings usually allow.

What exactly is inside a credit rating?

Because credit ratings is exhibited just like the several, it could be scary to ascertain what we provides if you will find zero reason behind review. It is such studying their marks at school. Credit ratings are not precisely anything we include in our societal news profiles both.

FICO Score

To have FICO, scores initiate at 300, towards the higher you to are 850. But, definitely, you can get no credit history anyway. Doing forty-five billion Us citizens may well not have a credit score now. It ensures that you don’t need to adequate credit history yet of creating a rating.

Constantly, it entails at least a couple of borrowing from the bank membership which have no less than six weeks off activity to find a precise photo. Your credit history usually contain all data compiled regarding as soon as you unwrapped your first borrowing account for the past percentage advertised by the a lending institution. Therefore it is you can to get differing ratings from more bureaus on other attacks.

Several situations sign up to the FICO Get. Chief of them points try the commission history. not, you should be aware that attract is heaviest toward study filed for the most latest period. For this reason, if you have generated a late fee before however it has been for enough time on expose, it really might not connect with their score as much as a good late commission you have made throughout your most recent asking years.

Comments :